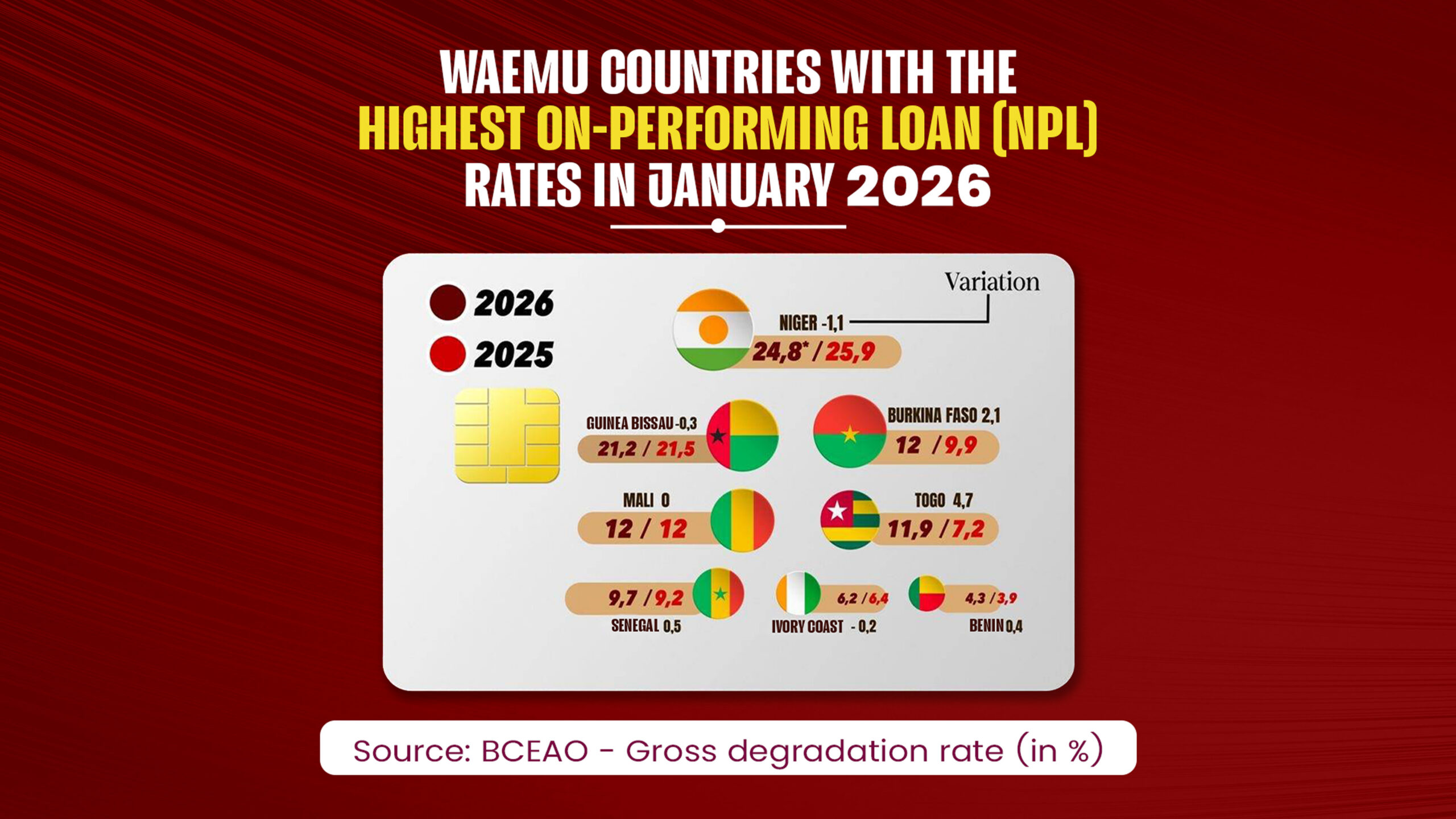

Niger leads uemoa’s rising bad loans crisis in 2026

An early 2026 economic outlook report reveals a troubling divide within the West African Economic and Monetary Union (UEMOA), where the banking sector’s growth is overshadowed by escalating credit defaults. At the epicenter of this financial storm, Niger stands out with the highest non-performing loan (NPL) ratio in the region, signaling deepening regional disparities.

Niger’s Banking Sector: A Record of Financial Distress

While UEMOA’s banking system grapples with structural challenges, Niger’s performance remains the most alarming in the bloc. Despite minor improvements, the country’s banking sector continues to lag far behind its regional counterparts in credit quality.

A Troubling Outlier

With an NPL rate of 24.8% in January 2026, Niger holds the unenviable position of leading the region’s default rankings. This means nearly one in four loans issued in the country is now in default, a figure that, while slightly lower than the 25.9% recorded in 2025, remains dangerously high.

Underlying vulnerabilities persist, driven by persistent security threats and political instability, which amplify the country’s financial fragility.

UEMOA’s Two-Speed Banking Reality

The January 2026 data underscores a stark divide between coastal economies and those in the Sahel, where financial instability is most acute.

Sahelian Economies Under Strain

The Sahelian bloc, including Niger, Mali, and Burkina Faso, faces severe credit deterioration:

- Mali & Burkina Faso: Both countries report NPL rates of 12%, with Burkina Faso experiencing a sharp increase of 2.1 percentage points over the past year.

- Guinea-Bissau: Despite a slight improvement, its NPL rate remains critically high at 21.2%.

Coastal Resilience with Cautionary Notes

In contrast, coastal nations demonstrate greater financial stability, though isolated concerns persist:

- Benin: Leads the bloc with the lowest NPL rate at 4.3%, setting a benchmark for regional performance.

- Ivory Coast & Senegal: Maintain relative stability with rates of 6.2% and 9.7%, respectively.

- Togo: The exception in this group, with NPLs surging from 7.2% to 11.9%, a 4.7-point jump.

The Broader Credit Landscape: Growth Overshadowed by Risk

The total credit portfolio in UEMOA has surpassed 40.031 trillion West African CFA francs, marking a 4.7% annual increase. Yet, this expansion is clouded by growing defaults, which now total 3.631 trillion CFA francs.

A critical indicator of strain is the coverage ratio, which has dropped to 59%. This suggests banks are struggling to keep pace with provisioning for bad loans as defaults accelerate.

Banks Retreat from Risk

Faced with deteriorating credit conditions in high-risk countries like Niger, financial institutions are adopting stricter lending practices:

- Stricter lending standards: Higher down payments and more stringent collateral requirements are now common.

- Selective credit expansion: Banks prioritize balance sheet safety over lending growth, potentially curbing funding for local small and medium-sized enterprises (SMEs).

As 2026 unfolds, UEMOA’s banking sector finds itself at a crossroads. While systemic stability is not yet in question, the financial distress in Niger and its spread across the Sahel demand heightened vigilance to prevent a potential liquidity crisis from engulfing the region.